Social Security- What You Need to Know Before You Claim

The key to good decision-making is about putting the odds in your favor. There are very few sure things in this life; the best we can do is make educated decisions. We choose not to smoke, eat healthily, or exercise, not because it guarantees that we won't have health problems but because it increases our odds of living a long and healthy life. We should look at claiming Social Security and most other financial and retirement decisions in the same light. In this article, I will lay out several ways you can put the odds in your favor when claiming Social Security retirement benefits.

The Basics

To make a good decision when it comes to claiming Social Security benefits, you first need to understand the basics of how it works. Retirement benefits are monthly payments that are paid to those who have paid into the Social Security System for 40 quarters (i.e., an accumulated ten years) or more. You pay into the system through FICA taxes that are deducted from your paycheck as an employee or through self-employment taxes for people who are self-employed. The Social Security System uses your highest 35 working years (adjusted for inflation) to calculate your retirement benefit. The higher your average income is, the more you are entitled to receive in monthly benefits.

Those who are entitled to benefits can claim those benefits early, on time, or late. First, let's define what on time means. On-time is your "Full Retirement Age" (FRA). The year you were born determines your FRA. Take a look at the chart below to see at what age you can claim your FRA benefit amount. You can also claim your retirement benefits as early as 62 or as late as 70.

All other things being equal, the longer you delay benefits, the higher your benefit will be for life. This increase in benefit is calculated on a monthly basis. In other words, for every month you wait to claim benefits, your monthly benefit amount will increase. Take a look at the graph below, and you will see how benefits increase over time if you delay. For all of my examples below, I am going to assume an FRA of 66.

Source: Social Security Administration (www.ssa.gov). Assumes full retirement age of 66 and individual born in 1943 or later. As of 2014

To understand what this equates to in dollars, see the chart below.

The Importance of Longevity

As you can see, your benefits increase substantially by delaying. This is only half of the story, though. Let's say you decide to delay your benefits until age 70 rather than taking them at 62, and then you pass away at 72. Was it a good decision to delay benefits for eight years (62-70) to get two years of higher benefits? The answer, of course, is "No!" If, on the other hand, you live to age 90 or 95, you will have received 20 or 25 years of significantly higher payments. You could make a strong case for delaying benefits in this situation.

A comment I often hear when explaining this previous scenario is, "Well, none of us know when we are going to die." That is true, but this would take us right back to the fundamentals of good decision-making. It is all about putting the odds in your favor. When faced with the decision to claim or delay benefits, I would encourage you to take a hard and objective look at your health, lifestyle, and longevity in your family. If you are in great health and have had several family members live into their late 80s and beyond, you should probably lean towards delaying benefits. If, on the other hand, you are in poor health and/or have poor longevity in your family, you may want to consider claiming early.

Cost of Living Adjustments

Cost of Living Adjustments are another reason to consider delaying retirement benefits. In a typical year, your Social Security benefits are increased by the approximate inflation rate for the previous year. This is called a "Cost of Living Adjustment" (COLA) increase. A COLA increase of 2 or 3% may not seem significant, but if you compound those increases over a 20 or 30-year period, they become very significant. The reason I say that COLA is another reason to consider delaying benefits is that a 3% increase on $1,320 over 20 years is a lot more than a 3% increase on $750 (dollar amounts are from the above example).

‘Til Death Do Us Part - Spousal Benefits

Spousal benefits are often overlooked and misunderstood but can be beneficial for some couples. In 1939, spousal benefits (along with others) were added to the Social Security System. At the time, most families had one working spouse and one stay-at-home parent. Our country’s leaders realized that the stay-at-home spouse provided a significant benefit to society and wanted to make sure they were not left out. That is why we have spousal benefits.

Spousal benefits allow you to receive an amount up to half of what your spouse is receiving without reducing what your spouse gets. It essentially allows you to get the higher of your benefit or half of your spouse's as long as you and your spouse have been married for one year or more and your spouse has already filed for benefits.

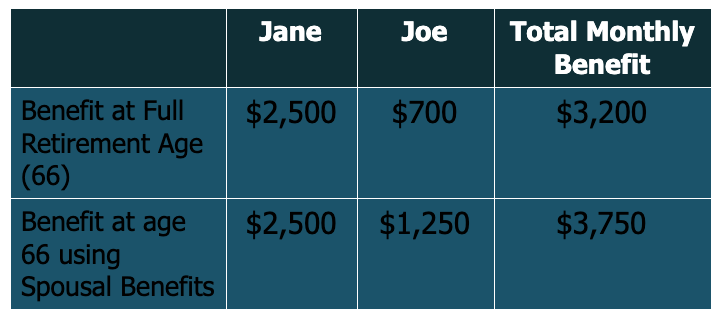

Let's take a look at a specific example of how this can work. Jane and Joe Jones are a married couple. Jane was a professor at a local university, and Joe stayed home to raise the kids but also worked as a substitute teacher. Since Jane's wages were higher than Joe's, the benefit she is entitled to is also higher. Jane is entitled to $2,500/month at FRA and Joe $700/month. Since half of Jane's benefit is more than Joe's full benefit, Joe would draw $1,250/month (half of Jane's benefit) rather than $700 (his own benefit). That’s an increase in income of $550/month for as long as Joe and Jane are both living! Over a 20-year period, that is $132,000 in additional benefits received, not including inflation increases!

When Death We Do Part

It is also very important to understand what happens when a spouse passes away. If you and your spouse are both receiving Social Security Retirement Benefits and one of you passes away, the surviving spouse gets the higher benefit but not both. The lower benefit will no longer be received. This is important for two reasons: First, there will be a reduction in income at the death of the first spouse and this should be planned for. Second, this means the higher benefit lives on as long as either one of the spouses is living. Going back to our longevity conversation, two people have a longer life expectancy than one person, which means whoever has the higher benefit should be the one who considers delaying since the higher delayed benefit will live on as long as either spouse is alive. This also means that if you are married, you should not only pay attention to your health and longevity but also your spouse’s. Even if you are in poor health, you may want to consider delaying benefits, especially if your spouse is in good health and you have the higher benefit.

Taxes and Penalties

If you are still working and under Full Retirement Age (FRA), you should be very careful claiming benefits. Not only will you receive a reduced benefit for claiming early, you also may have to pay taxes AND a penalty. In 2025, those who are under FRA and have earned an income of over $23,400 will have a penalty applied to their Social Security benefits unless their FRA is in 2025 then, the income cap is $62,160 for the months before they turn FRA. If you choose to start receiving benefits prior to FRA but will be FRA later in the year, you will want to take a look at additional resources like the following link: https://www.ssa.gov/benefits/retirement/planner/whileworking.html#:~:text=In%202020%2C%20if%20you're,full%20retirement%20age%20is%20%2448%2C600. This penalty can be significant and can even wipe out your Social Security benefits altogether if your earned income is high enough.

It is also important to understand what earned income is. It is typically wages earned through a job or self-employment income earned through your effort. Passive income (e.g., pension and investment income) does not count against the $18,240. Furthermore, once you are at Full Retirement Age, there is no limit to what you can earn. Even if you have a job that pays six figures, you will not be penalized as long as you are FRA.

Other Benefits

Below are a few additional features/benefits that are offered through the Social Security Retirement System. However, it is outside the scope of this article to dive into details on these. If you think one of these situations may apply to you, I would encourage you to seek the advice of a financial advisor who is competent in Social Security Planning.

Divorced Spouse Benefits: If you were married for ten years or more, have been divorced for at least two years, and have not remarried, you may be eligible for Divorced Spouse benefits. These benefits look and act a lot like spousal benefits.

Widow/Widower Benefits: If your spouse has passed away and you have not remarried, you may be eligible for Widow benefits. These can be powerful benefits and should be carefully considered.

Minor Children Benefits: If you are 62 or older and have minor children (adopted or biological), each of your minor children could be eligible to get an amount up to half of your benefit until they are 18 years of age.

Disabled children: A child with a disability may be eligible for 50% of your benefits if they were disabled prior to 22 years of age. Benefits may continue as long as your child is considered disabled.

Summary

As you have probably realized by now, determining when and how to claim Social Security benefits can be a complicated decision. To complicate it even further, we have the concept of opportunity cost. Opportunity cost is the cost associated with choosing one option over another. If you decide to delay claiming Social Security and instead take larger withdrawals from your investments, you are experiencing opportunity cost. Any extra withdrawals you need to take to allow you to delay Social Security will no longer be invested in your portfolio and will no longer be growing. All of this complexity has brought me to the conclusion that most people will benefit from working with a financial planner who is proficient in retirement planning and uses reputable financial planning software (i.e., e-money or money guide pro). Additionally, I would suggest the financial advisor you work with have either the CERTIFIED FINANCIAL PLANNER(R) (CFP(R)) and/or Chartered Financial Consultant(R) (ChFC(R)) certifications.

View more related content below:

https://fsgmichigan.com/vlog/true-finance-let-them-fly

https://fsgmichigan.com/blog/investing-to-and-through-retirement

This commentary on this website reflects the personal opinions, viewpoints and analyses of the Financial Strategies Group, Inc employees providing such comments, and should not be regarded as a description of advisory services provided by Financial Strategies Group, Inc or performance returns of any Financial Strategies Group, Inc Investments client. The views reflected in the commentary are subject to change at any time without notice. Nothing on this website constitutes investment advice, performance data or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Financial Strategies Group, Inc manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

Written by Brandon Carter