The Death of the Stretch IRA

The SECURE ACT was enacted on January 1, 2020. While it has been a few years since the act was passed, the effect of the largest retirement reform since 2006 is still being felt today. One of the major changes was the implementation of new required minimum distribution (RMD) rules for inherited IRAs. I like to call this the death of the Stretch IRA. First, let’s establish that an inherited IRA occurs when a loved one or family member dies with money left in their IRA, 401 (k), or even 403 (b), and you are named as a beneficiary. The funds are passed on to you through a vehicle called an Inherited IRA.

The SECURE ACT was enacted on January 1, 2020. While it has been a few years since the act was passed, the effect of the largest retirement reform since 2006 is still being felt today. One of the major changes was the implementation of new required minimum distribution (RMD) rules for inherited IRAs. I like to call this the death of the Stretch IRA. First, let’s establish that an inherited IRA occurs when a loved one or family member dies with money left in their IRA, 401 (k), or even 403 (b), and you are named as a beneficiary. The funds are passed on to you through a vehicle called an Inherited IRA.

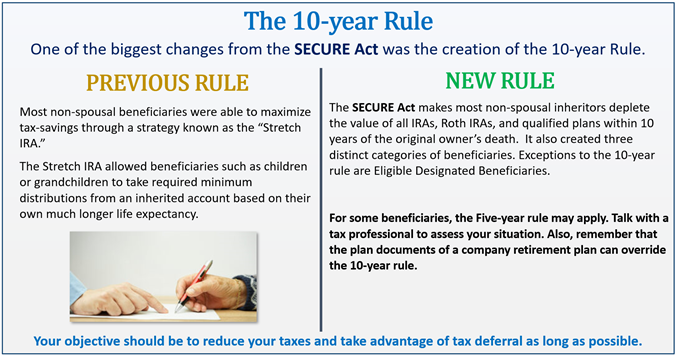

Why is the RMD change important? Before the passing of the SECURE ACT, any non-spouse beneficiary of qualified money could inherit assets and effectively “stretch” their RMDs out over their lifetime. From a tax perspective, this is very important as it allows for smaller annual distributions, reducing the overall tax impact of inheriting retirement assets. In addition, the stretch aspect of RMDs allows for planning and flexibility over a very long period of time. Post SECURE ACT, beneficiaries who inherit retirement assets from the original owner who was of RMD Age will be required to take RMD's annually. If the original owner was not of RMD age, they are not required to take annual RMD's. In both scenarios, the Inherited IRA is required to be depleted within 10 years of the original owner's passing. This can be problematic and complex, especially for those who are inheriting substantial assets or already have a healthy income.

How does this affect me? From a planning perspective, developing distribution strategies for the new 10-year rule has made everything more complex for the individual investor. When do I take distributions? How much do I take? How is the market performing? How does this impact my tax obligation? How does this fit into my own financial plan? The days of annually calculating your RMD and simply satisfying it each year are a thing of the past.

While there are still some exceptions to the 10-year rule, which allows individuals to stretch their inherited IRA. Such as a surviving spouse, minor children of the account holder, disabled or chronically ill, and individuals who are not more than 10 years younger than the deceased IRA owner. The rest of us will have to abide by the 10-year rule. With an estimated $ 49.1 trillion in retirement accounts as of 12/31/25 (1), this problem is only going to get much larger. The early Baby Boomers are starting to enter their later years, and by 2030, the entire Baby Boomer population will be 65+. The wealth transfer to the next generation will be massive, and without proper planning, much of that wealth could be chewed up by taxes.

This massive reform to Inherited IRAs has effectively ended the ability to “stretch” out Inherited IRA distributions for what could be multiple generations to a finite period of 10 years.

- https://www.ici.org/statistical-report/ret_25_q4

Written by: Kyle Cooper