First Quarter Market Update 2026: Catching Our Breath After the Threepeat

In my final update of 2025, I wrote about "The Year of the Threepeat," celebrating an incredibly rare market milestone: three consecutive years of double-digit S&P 500 growth. It was a strong period of market performance that padded portfolios and kept spirits high. However, if you’ve been paying attention to the headlines—or checking your accounts over the last three months—you know that the first quarter of 2026 has brought us some unwelcome volatility.

I often rely on analogies to explain market behavior, so think of Q1 2026 like a marathon runner immediately after crossing the finish line of a personal best. The runner doesn't just keep sprinting; they have to stop, catch their breath, and let their heart rate return to normal. After the historic sprint of 2023, 2024, and 2025, the market is currently catching its breath. We expected some breath-catching in 2026, but the reasoning was not quite on our bingo cards.

The War In Iran

As we often say, it's the unknowns that rattle markets. In this case, the unknown factor has been and continues to be The War in Iran. The outbreak of the war in Iran and the subsequent closure of the Strait of Hormuz in March 2026 triggered a historic energy shock, sending Brent Crude Oil surging past $120 a barrel.

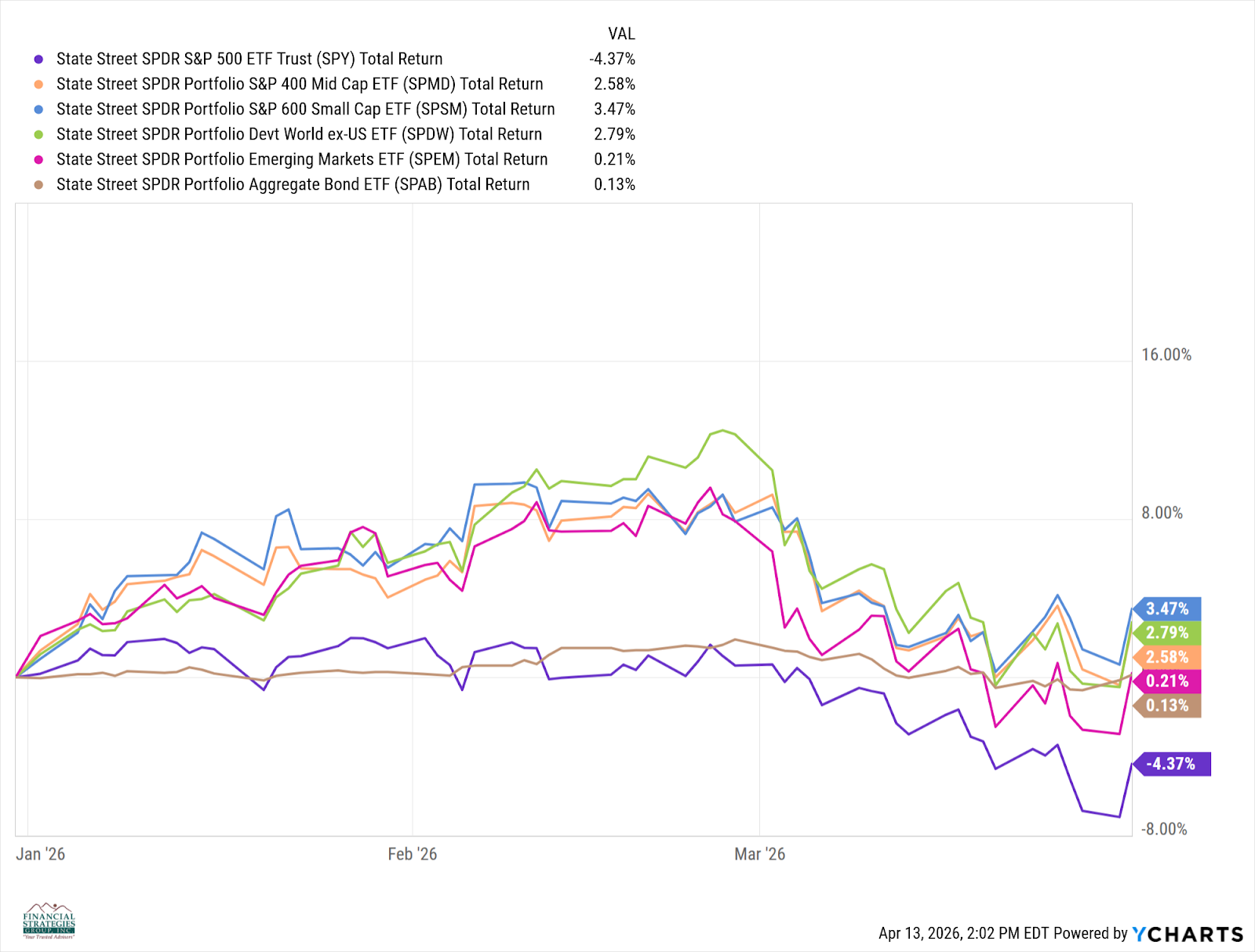

As you can see below, the markets started the year with relatively strong performance; however, with the start of Operation Epic Fury at the end of February, markets experienced a “grande” or medium-sized sell-off.

You’ll notice that the worst performing asset class is US Large Cap stocks, aka the S&P 500. Going into 2026, we were most concerned about the valuation of this sector, which, in turn, was a valid concern. Although we may not know when these types of world events occur, we do know that the most overvalued asset classes are typically hit the hardest by them.

This is where our philosophy of global diversification comes into play. Not only do the majority of our portfolios own emerging markets and international developed stocks, but we also have small biases towards mid and small sized stocks as well. These diversification elements are definitely helping weather the volatility we have witnessed this year.

You don’t hire us to be geopolitical experts, and I won’t pretend to be one. I have no idea when this situation will end, although we certainly hope for a quick resolution. We do believe markets will experience an exuberant rebound when the crisis is resolved.

The Performance Breakdown

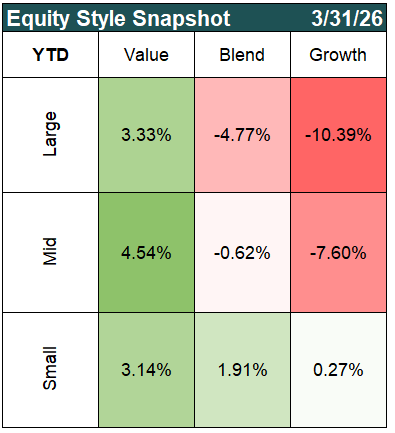

Put simply small cap and value stocks have outperformed their growth and large cap peers.

Energy is certainly a contributor to the outperformance of value; however, the excess spending on AI by many tech, software, and communication stocks (aka growth companies) is starting to be questioned. This contributes to the selloff in many of those companies. Obviously, the spending on AI will produce some efficiencies for these companies, but when volatility hits, investors start to question when those efforts will produce those efficiencies.

Looking Forward

If The War In Iran and its impact on the oil market continue for a prolonged period, higher oil prices could contribute to increased inflation. Oil/energy prices impact the cost of every good and service we use. Frankly, we cannot have sustained high oil prices without the impact bleeding into everyday spending and therefore the economy.

A prolonged conflict in Iran could increase the risk of broader economic impacts, including slower growth.

Another major market impact to keep our eyes on is the Federal Reserve. We will be getting a new Fed Chair (likely Kevin Warsh). It will be interesting to see how Mr. Warsh approaches interest rates now that he has been nominated by President Trump. Early indications and the belief on Wall Street are that Mr. Warsh will be in favor of the President’s insistence on cutting interest rates.

We believe that the Fed does need to remain independent; however, lower interest rates are likely a positive for the stock and bond markets as long as this does not lead to a higher and ultimately unsustainable inflation rate. Time will tell!

As always, if you have any questions or concerns, please reach out to your advisor. Say hello to Spring, my friends!!!

Written by: Brice CarterThis commentary on this website reflects the personal opinions, viewpoints, and analyses of the Financial Strategies Group, Inc employees providing such comments, and should not be regarded as a description of advisory services provided by Financial Strategies Group, Inc or performance returns of any Financial Strategies Group, Inc Investments client. The views reflected in the commentary are subject to change at any time without notice. Nothing on this website constitutes investment advice, performance data, or any recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Financial Strategies Group, Inc manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.